Basic Financial Planning for Start-Up Workers: Your Goals

This is Part I in what will hopefully be a multi-part series on how start-up workers should best manage their financial planning. For more about me and caveats, see the intro. I obviously don’t know you (or maybe I do, but still…), so please think critically about your personal situation before making decisions with your money.

Step 1: Write down your goals

The cornerstones of all financial planning are your goals. Why, exactly, are you saving money?

For most of us, our goals follow the same general pattern. But small differences in what we want can make for wildly divergent steps that we need to take.

So before anything else, you need to think about what you are trying to accomplish. Write down your goals in roughly the order of importance to you. And by ‘goals’ I mean ‘anything that you have to save for’.

Here are mine:

1. I want to support myself and hopefully, a wife, through my retirement and not require resources from my family or the government

2. I want to be financially prepared for a situation where I do not earn an income for two years

3. I want to be able to support my immediate family if someone needs financial help

4. I want to be able to pay for my (potential) children to go to college wherever they want

Those are my goals. Yours may be different: they may involve starting a company, traveling around the world, leaving money to your alma mater, swimming in a giant pool of money, whatever. One thing that most people would as a goal is a down payment on a house: I’m not so interested in that myself though if I change my mind about the relative value of owning a house I may reconsider.

Once you have written down your goals, you want to estimate what each of those things will cost, in today’s dollars. This is fairly straightforward*: do it in two parts. First, everything other than retirement: these are modified from my actual numbers to be closer to averages for my age, and what college costs. Do this for yourself:

I’m pretty conservative here, especially with the college assumption, but in general I want to have about $630k to pay for these things (in today’s dollars). That looks like a gigantic number, but over a 20 year horizon, with two incomes and hopefully some investment gains, that’s not too crazy to hope for: if I have any luck at all investing, if we each sock away about $10,000 per year we’ll be in great shape.

The big issue, obviously, is retirement. How long will your retirement be and how much money will you spend? Standard estimates are 30 years and 75% of your income.

I’m not prepared to get into a really in-depth discussion of retirement, since it is so complex and certain issues (like: what will social security look like in 20 years?) are important and almost impossible to know. Investment lore is that you can spend 4-5% of your savings every year and it will last for 30 years in any market. Put another way, you should have 20-25x your annual expenses saved up. So if I think I could happily retire with $50,000 of annual expenses (for two of us, hopefully), I would want $1-$1.25 million (in today’s dollars, again) in my savings.

At least one Nobel Prize winner thinks the 4% rule isn’t great, and historical returns indicate that 4% is maybe being overly safe. As a simple rule, however, I think it is pretty reasonable**.

Regardless, a lot of this is very ‘big-picture’ and probably doesn’t help with your immediate decisions about: where should I invest? That will be in the next part of this series.

*Total lie- this is not straight-forward at all. A financial planner would consider the expected inflation, expected return, and time-value of money in these calculations. Of course, the planner doesn’t actually know what the inflation and expected return will look like. The additional complexity of their models, in my opinion, is not especially valuable at this stage of planning, so don’t sweat it.

**For finance nerds: I know there is a lot of math that can be done around optimizing savings, concerning relative returns and portfolios construction and how they relate to Roy’s Criterion or other decision models. My experience is that additional math here just turns into an argument about assumptions and isn’t very useful, though often fun to discuss.

Basic Financial Planning for Start-Up Workers: Intro

So it’s early in the year. Maybe you’re the type to make New Year’s resolutions. Maybe you’re the type to make New Year’s resolutions and then wake up on the floor still wearing a glasses that spell out 2012.

Regardless, it’s 2012, and you have to settle up with Uncle Sam. You either have a K1 or W2 or you will soon.

This is the time where most of us figure out our finances for the year. You have a few months to figure out how to pay your taxes and make contributions to an IRA retroactive to 2011. And if you’re making contributions to an IRA or 401(k), you may need to figure out what fund to put your money into.

Confused?

Right now you’re every financial marketer’s dream. You have money you need to put somewhere and very little sense of differentiation between your financial options. You’re looking for the answer via Google or your buddy in finance, but the answers from Google are vague and conflicting and your buddy doesn’t really want to take responsibility for you. And most importantly, no one really is accounting for your specific situation- you’re smart, you’re young, you’re working at a small company and you have no idea what’s coming next.

Who am I and why am I writing this?

I am the finance friend for a few people in NYC. I have some friends who ask for advice, which I try to give, but I know it’s in one ear and out the other. Some things are better communicated in writing. People generally start yawning as soon as I mention adjusted gross income, so I figured having it on paper (er, screen) would probably help them/everyone out.

More importantly, I’m a transplant from finance into tech. Everyone I have met in the start-up world has been incredibly nice to me and eager to help me out. This is one place I honestly feel like I can give back, so I’m going to try to make this as not-awful as I can.

Am I qualified?

I hope so. I worked in finance jobs for about 7 years, in a variety of analytical positions. I manage money for myself and some family members. I helped create Lumesis, a software company that provides information about the bond market to larger institutional investors. I’ve also co-written a book on financial simulation, which I admit is not 100% applicable for individual planning.

Finally I was a CFA charterholder, which means that I passed three tests on the financial markets and worked in finance for at least 48 months. In the NYC finance world, people who have passed the CFA exams are generally regarded as excel monkeys with the social skills of 16-year-old Mathletes. In a related story, I wrote 750 words about the decline of the Walkman. Last month. If you are interested in more about me, see here.

Of course, the one way that I’m not qualified to advise you is that I don’t know you or your financial situation. Please consider your situation and your goals before making any decisions. Also, talk to your doctor before starting any diet or fitness regimen. And eat your vegetables.

Who are you?

I’m writing this for people who fit the following buckets:

-In the US or subject primarily to US tax laws

-Young (under 40 counts, unless you want to retire at 45)

-You don’t have a lot of clarity into your future earnings: you might have no need to plan because your company is going to be worth more than the GDP of Madagascar, or you could be drowning your sorrows in the same bar as the pets.com guys. (Note: the downside risk applies to most people: they just don’t realize it).

-You don’t own your home

-You have some amount of your net worth tied up in options or equity

If this describes you reasonably well, hopefully the posts I’ll be putting up over the next week or so will be helpful to you. Part I coming tomorrow..

Real Life Atlantis

Atlantis was a legendary island that sank beneath the waves, according to Plato.

While many have searched for it, the story of the island is generally believed to be fiction.

However, I learned today that in the modern era, there was an island instantaneously lost. Or, more accurately, blown up.

In 1952 the US government tested the first nuclear fusion bomb, ‘Ivy Mike’ on the island of Elugelab in the Enewetak Atoll. The bomb was so powerful it reduced the island to an underwater crater that was visible from space.

This is what the atoll looked like before;

and this is what it looked like after

as Wikipedia (source for these photos) puts it ‘note crater on left’.

People Don't Fart Like They Used To: More Fun with N-Grams

In playing around with N-Grams on Monday, I noticed that the use of the word ‘fart’ has declined precipitously over the last three centuries.

I was very excited about this, thinking I has just made a major discovery about the history of indigestion.

Unfortunately, digging into the data shows that this is due errors in Google’s OCR.

Clearly these are mis-readings of the word ‘part’. Though the biblical passage is arguably improved by the replacement.

Dying Words: More Fun with N-grams

One of the great things about being in the start-up world now is the excitement around creating something new. All around me people are excited about what they are doing in a way that I haven’t seen since I was in finance at the height of the bubble. And though I’m wary since I’ve lived through a bubble burst, I share the optimism.

But I miss the things that are going out of style. Not in an ironic way, like some people cherish mustaches moustaches, but because I’m sad that some people won’t know the world the way I know it. It is possible to lose technology or language completely. No one knows how to make Damascus steel or speak Linear A anymore.

So this is a tribute to some of the words or concepts that are leaving the English language. All of these words have seen their usage reduced by more than half since their peak, as measured by the always entertaining Google N-Gram Viewer.

Old Technology

As computer word processors continue to kill off the typewriter, it’s no surprise that the word is used less and less.

But changes in physical technology aren’t the only thing that can become obsolete. There are less than 20 ‘true’ monarchies left in the world

Changing Tastes

Sometimes objects just gain negative connotations and fall out of style. Even if you still need them to make a good pie crust.

And Other Reasons

Sometimes it isn’t totally clear why words fall out of favor. I think of the words ‘peculiar’ and ‘remarkable’ as words from the 19th century. And they are. But I can’t think of why. Fortunately, both words seem to be making a comeback (thanks, Brooklyn!).

If you have any ideas that explain the peculiar paucity of the word peculiar, or the remarkable decline in the word remarkable, let me know.

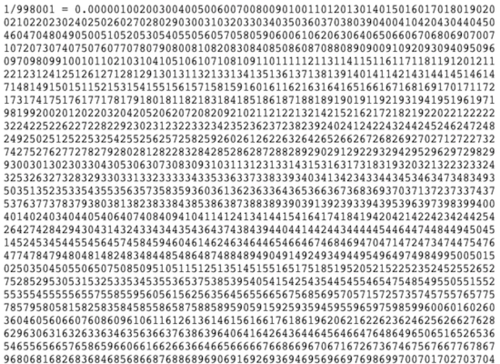

I Heart Chaos: Fun with math: Dividing one by 998001 yields a surprising result

I Heart Chaos: Fun with math: Dividing one by 998001 yields a surprising result

There’s all sorts of magic to be had with numbers, and many mathematicians have made entire careers in finding these little tricks that are mostly useless, but fun anyway. Unfortunately, a lot of calculators are going to truncate the results of this trick, but if you manage to get a hold of one that doesn’t, solving 1/998001 will generate all the three digit numbers from 000 to 999. And in order, no less. If you’re a fan of this kind of math fun, solving 1/9801 will generate all the consecutive two digit numbers.

Noise Machine

I no longer work in finance, but I have a lot of friends who still do. Most of them aren’t that happy right now- they don’t feel very secure in their jobs. And I don’t blame them. But I don’t see a ton of them getting let go. The axe is perpetually hanging over their heads, but never drops.

I think a lot of the reason for insecurity is the obsession with labor issues in the financial press. Bonus season coverage is only fractionally less intense than coverage of the Oscars, as far as I can tell. Relatively minor layoffs end up getting amplified to an extent that I think is utterly ridiculous.

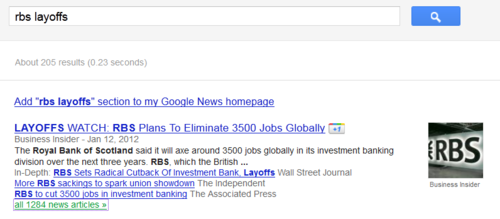

Last week RBS announced layoffs of 3,500 workers (out of about 19,000). That’s fine- everyone has known that RBS is in bad shape. I wanted to read about it (I have friends there) so I checked it on Google News.

To my shock, there were over 1,200 articles about it last week! that’s an article for every three people cut!

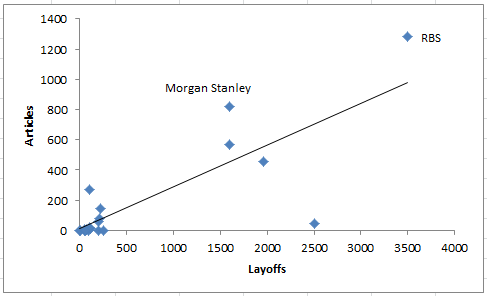

I guess that the papers have to work with whatever is in the news, but I still thought that was high. So I did a Google News search for layoffs over the past month to see how much coverage each set of layoffs got. The X axis is the number of layoffs, the Y is the number of articles

I labeled Morgan Stanley & RBS. Not only are they the most covered on a per-layoff basis, but they’re the most covered absolutely as well.

So cheer up, finance people. It’s (probably) not that you’re more likely to get fired: it’s that you’re more likely to hear about it. Many, many times.

[gallery]

Many of you have asked, so here’s what’s going on with me.

WHAT HAPPENED BEFORE

- 8/1979: Born. Grew up in CT, built a killer eraser collection, fell in love with computers.

- Left college to start a company. Fell hard. Fled to India for 3 months.

- Started 2nd company. Learned to be an adult. Fell in love with NYC.

- Moved to SF, discovered burritos & some of my fave people on Earth.

- 9/2011: Got diagnosed with Leukemia!

- Cried. Went through 3 cycles of chemo. Hurt. Thought hard about what I want out of life. Grew up a second time.

TODAY

… After over 100 drives organized by friends, family, and strangers, celebrity call-outs, a bazillion reblogs (7000+!), tweets, and Facebook posts, press, fundraising and international drives organized by tireless friends, and a couple painful false starts, I’ve got a 10/10 matched donor!

You all literally helped save my life. (And the lives of many others.)

WHAT HAPPENS NEXT

Tomorrow, I’ll be admitted to Dana Farber in Boston for 4-5 weeks.

First I’ll get a second Hickman line to allow direct access to my heart (for meds and for nutrients if I’m not able to eat). Over the next week, the docs blast my body with a stiff chemo cocktail to try and eradicate all traces of cancer cells. In the process, the immune system I was born with, and my body’s ability to make blood, are destroyed.

Next Friday, I get my donor’s stem cells by IV. I start on immunosuppressants to prevent my body from rejecting them (I’ll be on them for 12-18 months). For these weeks I’ve no immune system, so I’m severely vulnerable to viruses and bacteria. My hospital room and hallway become my world.

Meanwhile, the stem cells make their way to my bone marrow and, with some luck, start producing platelets, red blood cells, and white blood cells. At this point, my blood type changes to the blood type of my donor. And my blood will now have my donor’s DNA, not my own.

This is science fiction stuff. I can hardly believe it’s even possible, and there’s lots of chances for things to go wrong. It’s frightening.

AFTER THE TRANSPLANT

Recovery to a new state of “normal” takes about a year, but there’s a few storm clouds hovering:

- My immune system is new, like a baby’s. I’m prone to getting sick.

- Just as with any organ transplant, there’s a chance of rejection. Except in this case, it’s my blood that’s the foreign body, and it touches every organ. They call it graft-vs-host-disease and it can cause health issues and organ complications for the rest of my life.

- Successful transplant or not, Leukemia can relapse. Stubborn mofo.

Overall, 75% of AML transplant patients survive year one, 50% make it through year five. My odds are a little better since I’m young.

THE GREAT NEWS

I’ve got a long road ahead. But I’ve got a donor & amazing family & friends. A few months ago I didn’t have many options. Today I have a plan.

I am alive. I start tomorrow. Wish me luck!

Thank you.

Awesome news. Really, really excited to see. Congrats to Amit and his family, and everyone at SAMAR and everywhere else who made this a possibility.

More Fun with N-grams: Shak(e)speare

I saw Richard III at BAM on Friday, which was outstanding. While I was playing around with the N-gram viewer yesterday, I tested some of the spellings of his name and discovered that the spelling we use today only became the popular spelling during the civil war:

I looked into it before Wikipedia went dark, and apparently there is no record of the man ever spelling his name with the first ‘e’. The six signatures appear as follows:

- Willm Shakp

- William Shaksper

- Wm Shakspe

- William Shakspere

- Willm Shakspere

- By me William Shakspeare

Notice the conspicuous absence of the first ‘e’.

I was trying to figure out why the shift to ‘Shakespeare’ happened. Strangely, it seems that British Prime Minister Benjamin D’Israeli might have been the catalyst for the change- he is the only influential person mentioned around that time having strong opinions. By the time of his death in 1881, the spelling ‘Shakespeare’ was preferred 3:1.

Does anyone have any other ideas on why this change happened?